Are you curious about What is Blockchain Technology and How It Works? Discover its wide-ranging applications, from revolutionizing voting systems to securing intellectual property and enhancing supply chain transparency across industries. So, let’s dive deep to explore this topic.

What is Blockchain Technology?

Blockchain technology is like a special digital book that keeps track of transactions and makes sure they are real. It is very safe because it doesn’t need middlemen, and everyone can see what’s happening. It helps us trust each other more and makes things work faster and better. It can change how businesses work and keep our money and things safe.

Blockchain technology is very popular and important. It changes many industries and makes them better. It removes the need for middlemen and makes transactions safe and trusted. It can be used in finance, supply chain, and healthcare to make things better. Blockchain is making big changes and is very important in the digital world.

Understanding Blockchain Technology

Who is The Founder of Blockchain Technology?

The founder of blockchain technology is credited to an individual or group known as Satoshi Nakamoto, whose true identity remains unknown. Nakamoto published the Bitcoin whitepaper in 2008, introducing blockchain as the underlying technology for the first decentralized cryptocurrency.

Definition and Core Principles

Blockchain is a special kind of digital record that keeps track of transactions. It doesn’t need a central authority and everyone can see it. It helps us trust each other and makes things fair. Blockchain can change the way we do things by making transactions safe and fast.

Let’s see some core principles for better understanding:

Immutability: Blockchain ensures that once a transaction is recorded, it becomes nearly impossible to alter or delete, ensuring the integrity of data.

Transparency: All participants have access to the entire transaction history, promoting trust and accountability by enabling verification and auditing of transactions.

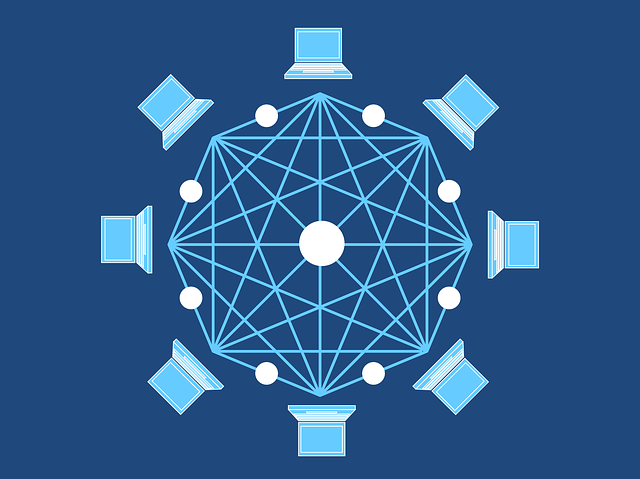

Components of a Blockchain

Blocks and Their Structure

Blocks are an essential component of a blockchain. They serve as containers that hold a set of transactions and other relevant information. The structure of a block typically includes the following elements:

- Block Header: The block header has important information about the block. It includes a special code called a hash, the time it was made, and a link to the previous block.

- List of Transactions: Each block contains a list of transactions that are included in the block. These transactions can involve the transfer of digital assets, smart contract interactions, or any other type of data exchange.

- Nonce: A nonce is a randomly generated number that miners modify during the mining process to create a hash value that meets specific criteria.

- Hash: The hash of a block is a unique identifier that is generated by applying a cryptographic hash function to the block’s header and transaction data. It serves as the block’s digital fingerprint.

The structure of blocks ensures the integrity and security of the blockchain. They’re connected like a chain using special codes called hashes. Once something is recorded in a block, it’s hard to change without changing all the other blocks. This makes the blockchain trustworthy and reliable.

Transactions and their inclusion in blocks

In a blockchain, transactions are like digital exchanges. People check and confirm them before putting them together in blocks. Each block has lots of transactions, making a chain. This keeps transactions safe, unchangeable, and easy to see for everyone in the blockchain network.

Cryptographic hashes and integrity

Cryptographic hashes are unique digital fingerprints generated by mathematical algorithms. They keep the data safe by checking if anyone changed it. The hashes connect blocks and make the blockchain secure.

Consensus algorithms

Consensus algorithms help people in a blockchain agree. There are different types like Proof of Work (PoW) and Proof of Stake (PoS). They make sure things are fair and secure. We also have Delegated Proof of Stake (DPoS) and Practical Byzantine Fault Tolerance (PBFT). These algorithms keep the blockchain trustworthy and safe.

How Blockchain Works Step-by-Step Breakdown

Transaction initiation, verification, block creation, and addition

The process of handling transactions in a blockchain involves several stages:

- Transaction Initiation: Blockchain technology starts with someone wanting to send or receive something. They make a digital record that shows who it’s from, who it’s going to, and what they’re giving or getting.

- Verification: When a transaction happens, it gets checked by people in the network to make sure it’s real. They check if the person sending it is allowed to, if they have enough money, and if it follows the rules or smart contracts.

- Block Creation: Verified transactions are grouped together into a block. The block is created by adding a unique identifier, timestamp, and reference to the previous block in the blockchain. Additionally, miners may compete to solve a computational puzzle (in Proof of Work) or take turns as validators (in Proof of Stake) to create the block.

- Block Addition: When a block is made, it gets added to the blockchain. The block connects to the previous block using special codes, making a chain of blocks. Everyone in the network agrees on the block’s correctness and where it goes in the blockchain.

The process of initiating transactions, checking them, creating blocks, and adding them to the blockchain makes sure that transactions are recorded securely. This happens in a clear and unchanging way.

Role of Miners and consensus algorithms

Miners check and add blocks to the blockchain. This keeps the network safe from fraud. Consensus algorithms make rules so everyone agrees on the blockchain. Miners and consensus algorithms work together to protect the blockchain and keep it secure.

Advantages of Blockchain Technology

Transparency and trust in transactions

Transparency:

- Blockchain ensures transparency by storing transaction data in a decentralized ledger accessible to all participants.

- All transaction details are recorded and can be audited by anyone in the network.

Trust:

- Blockchain fosters trust by eliminating intermediaries and relying on consensus mechanisms for transaction validation.

- The decentralized nature of blockchain reduces reliance on a single trusted entity.

- The immutability of blockchain data ensures the integrity and reliability of transactions.

Transparency and trust are inherent features of blockchain, providing participants with auditable and trustworthy transactions.

Security through cryptographic techniques

Blockchain ensures security through:

- Data Encryption: Encrypting sensitive data within transactions to prevent unauthorized access.

- Digital Signatures: Verifying transaction authenticity and integrity using cryptographic signatures.

- Hash Functions: Protecting data integrity by generating unique digital fingerprints for transactions.

- Consensus Mechanisms: Employing cryptographic algorithms to secure the blockchain network.

Blockchain technology uses special codes to keep information safe and make sure it’s real. This helps to protect data, make sure things are genuine, and stop anyone from changing them without permission.

Reduction of intermediaries and costs

Blockchain technology achieves cost reduction by:

- Peer-to-Peer Transactions: Enabling direct transactions without intermediaries, eliminating fees and delays.

- Smart Contracts: Automating transactions with predefined rules, reducing the need for intermediaries like lawyers or brokers.

- Decentralization: Removing the reliance on centralized authorities, reducing costs associated with their involvement.

- Streamlined Processes: Real-time tracking, auditing, and verification of transactions, reducing administrative overhead and reconciliation costs.

Blockchain makes things faster and cheaper by cutting out middlemen, simplifying how things are done, and saving money. It helps make transactions work better and cost less.

Potential for automation and smart contracts

Blockchain enables automation through smart contracts, providing benefits such as:

- Efficient and Trustworthy Automation

- Streamlined Operations

- Cost Savings

- Transparency and Security

Blockchain’s potential for automation and smart contracts enhances efficiency, reduces costs, and improves trust and transparency in business processes.

Use Cases and Applications

Blockchain technology benefits industries such as:

- Financial Services: Faster, secure transactions, cost reduction, and decentralized finance (DeFi). And cryptocurrency operates by blockchain technology.

- Supply Chain Management: Transparency, traceability, and efficient logistics.

- Healthcare: Secure sharing of patient data, interoperability, and drug traceability.

- Real Estate: Simplified property transfers, fraud prevention, and fractional ownership.

- Energy and Utilities: Peer-to-peer energy trading and transparent renewable energy tracking.

- Intellectual Property: Secure registration, ownership records, and royalty management.

- Voting and Governance: Secure and transparent voting systems and improved governance.

Blockchain revolutionizes industries by increasing efficiency and trust while reducing costs.

Challenges and Limitations

Blockchain technology has challenges and limitations. It can have problems with scaling and uses a lot of energy. There are also issues with rules and regulations, making different systems work together, and keeping things private. People might not want to use it because it’s hard to understand and can be expensive. It’s important to solve these challenges to make blockchain work well in different industries.

Some challenges and limitations are:

- Scalability

- Energy Consumption

- Governance and Regulatory Issues

- Interoperability

- Privacy Concerns

- Adoption Barriers

- Security Vulnerabilities

- Cost and Complexity

Conclusion

Blockchain technology holds immense promise in revolutionizing industries, but addressing its challenges is essential for unlocking its full potential and ensuring widespread adoption.

FAQ

FAQ: Frequently Asked Questions about Blockchain Technology

- What is blockchain?

– It’s a secure digital ledger that records and verifies transactions.

- How does it work?

– Transactions are grouped into blocks and linked together using cryptography.

- Is blockchain only for cryptocurrencies?

– No, it has applications in various industries beyond cryptocurrencies.

- Is it secure?

– Yes, blockchain is secure due to its decentralized and cryptographic nature.

- Can it be hacked?

– Hacking blockchain is highly difficult due to its decentralized structure.

- What are smart contracts?

– They are self-executing contracts with predefined rules for automated enforcement.

- Is blockchain scalable?

– Scalability is a challenge, but solutions are being developed.

- Are all blockchains the same?

– No, they differ in architecture, consensus, and decentralization.

- Is blockchain regulated?

– Regulations vary, with frameworks being developed for compliance.

- What’s the future of blockchain?

– It holds potential for industry transformation and ongoing advancements.